In the first post of this series, I argued that AI adoption needs both optimism and discipline.

The opportunity is real: AI can accelerate analysis, drafting, software delivery, customer support, fraud detection, and decision preparation.

The risk is also real: AI can be wrong, overconfident, inconsistent, and hard to audit if it is dropped into workflows without a clear operating model.

So the question is not:

How do we replace humans with AI?

The better question is:

How do we design human-AI workflows where each side does the work it is best suited to do?

The Core Principle

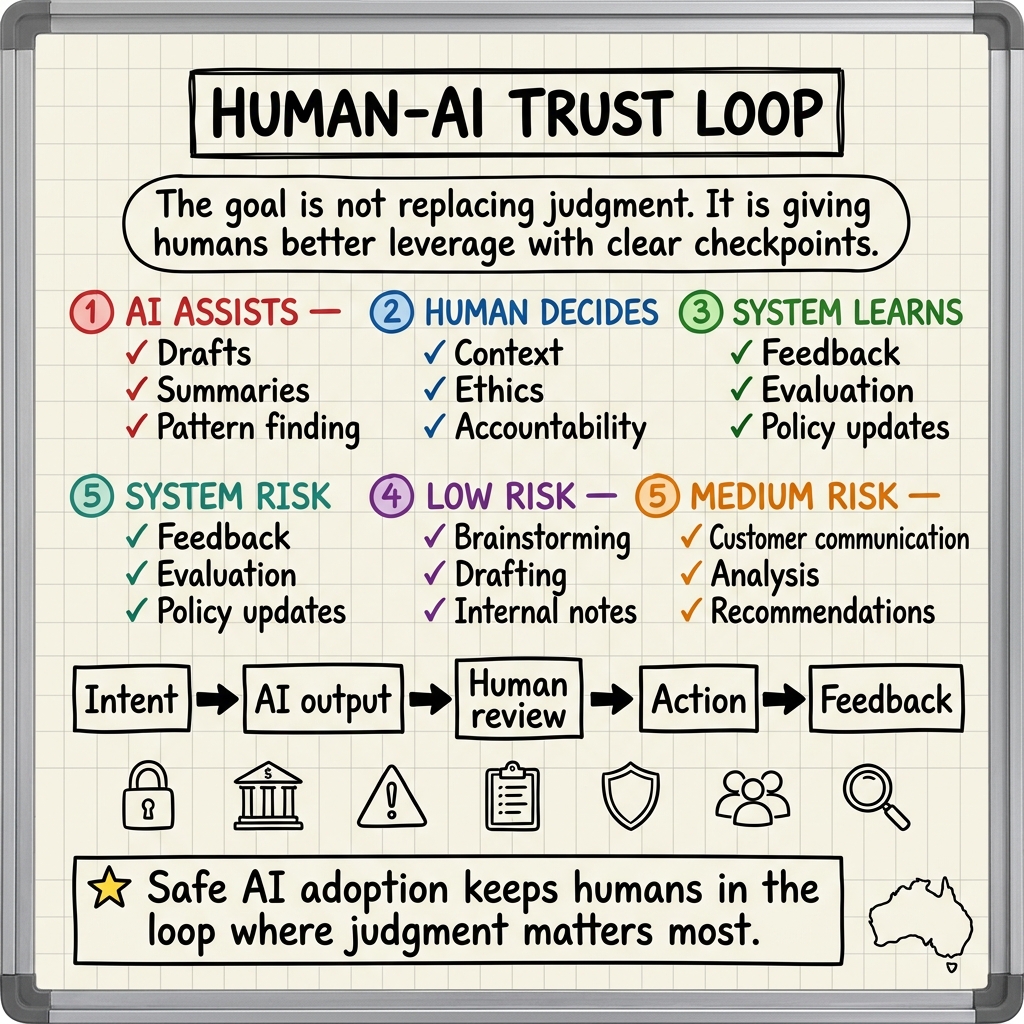

AI should expand human leverage without blurring human accountability.

That sounds simple, but it changes the design of every AI workflow.

| AI is good at | Humans are good at |

|---|---|

| Pattern recognition across large datasets | Understanding context and consequences |

| Drafting, summarising, translating, and classifying | Setting intent, values, and trade-offs |

| Monitoring high-volume signals | Handling edge cases and exceptions |

| Generating options quickly | Owning decisions in regulated or high-risk contexts |

| Finding anomalies and surfacing candidates | Deciding what action should be taken |

The goal is not to put a human rubber stamp on every AI output.

The goal is to route the right work to the right level of judgment.

A Practical Adoption Loop

The safest AI programs move through a loop of verification and learning.

- Identify the business problem. Start with a real workflow, not a technology looking for a use case.

- Assess data readiness. Check data quality, access, privacy, lineage, and permission boundaries.

- Run a narrow pilot. One workflow, one team, one owner, one measurable outcome.

- Build human oversight into the design. Do not add review after the workflow is already live.

- Measure business impact. Track time saved, error reduction, customer impact, risk reduction, or revenue protection.

- Decide whether to scale. Scale only if value and control are both proven.

- Keep verification layers. Monitoring, evals, audit trails, and human escalation remain part of production.

The loop is honest. It assumes many AI ideas will not work on the first attempt.

That is not failure. That is disciplined product development.

The Trust Boundary

Every AI workflow needs a visible boundary between suggestion and authority.

| Workflow risk | AI can usually… | Human should… | Required evidence |

|---|---|---|---|

| Low | Draft, summarise, brainstorm, classify internal content. | Review selectively and improve the output. | Version history and prompt/context record. |

| Medium | Recommend actions, prioritise work, prepare customer responses. | Approve before external or operational impact. | Source links, confidence signals, reviewer identity. |

| High | Detect fraud, flag compliance issues, suggest payment or account actions. | Make or approve the final decision. | Audit trail, policy mapping, case notes, escalation path. |

| Critical | Affect money movement, legal position, safety, access, or irreversible customer outcomes. | Remain accountable and explicitly authorise. | Full trace, reason codes, control checks, and rollback path. |

This boundary should not live only in a policy document.

It should be visible inside the workflow.

People should know when AI is suggesting, when AI is acting, when a human must approve, and what gets recorded.

Security And Well-Architected Gaps To Call Out

Human-in-the-loop design fails when the loop is vague. A human checkpoint only helps if the reviewer has context, authority, evidence, and time to make a real decision.

| Gap | Why it matters | Control |

|---|---|---|

| Human review theatre | Reviewers approve AI output without evidence or accountability. | Show sources, confidence signals, policy mapping, and reviewer responsibility. |

| Insecure output handling | AI output is copied into emails, code, customer records, or workflows without validation. | Treat AI output as untrusted until validated against the target context. |

| Weak identity model | The AI workflow acts with shared service credentials rather than user-scoped access. | Use least privilege, user attribution, and separable service permissions. |

| Missing audit trail | Teams cannot prove who approved what, when, and on what evidence. | Log prompt context, retrieved data, tool calls, reviewer, decision, and action. |

| No incident path | Incorrect AI actions have no rollback, escalation, or customer remediation path. | Define fallback, rollback, incident owner, and communication path before production. |

The Well-Architected gap is usually operational: the team designs a clever workflow but does not design the support model around it. A safe AI partnership needs operating procedures, measurable reliability, cost visibility, and security controls from the first pilot.

Evidence From Payments

Payments is a useful place to study human-AI partnership because the stakes are high and the data volume is enormous.

Visa’s Fraud Defence

Visa has used AI across fraud and risk workflows, including generative AI applications for specific fraud problems. The important lesson is not simply that AI detects more patterns. It is that human experts remain part of the governance and validation loop.

Mastercard’s Hybrid Model

Mastercard has invested heavily in AI and cybersecurity, using AI to accelerate analysis and identify potentially compromised cards. But acceleration is not the same as delegation. Human specialists still matter for decisions where customer impact, false positives, and operational consequences need judgment.

Swift’s Collaborative Approach

Swift’s work with banks on AI-enabled fraud detection shows the same pattern: AI learns from transaction data and historical patterns, while banking professionals validate how those outputs should be used.

The common lesson is clear.

AI creates leverage. Human judgment creates accountability.

What Good Human-AI Workflow Design Looks Like

| Design choice | Weak implementation | Strong implementation |

|---|---|---|

| Problem framing | ”Use AI for support." | "Reduce average case triage time by 25% while preserving quality.” |

| Review model | ”A person can check it.” | Review thresholds are based on risk, confidence, customer impact, and reversibility. |

| Feedback loop | Corrections disappear into chat history. | Human decisions are captured and used to improve prompts, rules, and evals. |

| Auditability | The final answer is saved. | Inputs, sources, tool calls, reviewer, decision, and action are traceable. |

| Scaling | Successful pilot gets rolled out broadly. | Pilot graduates only after value, safety, and operating ownership are proven. |

The Three Questions To Ask First

Before starting an AI pilot, ask:

- What decision or output are we improving?

- Who is accountable when the AI is wrong?

- How will we know the workflow is safer, faster, or better?

If the answer to any of those questions is vague, the project is not ready to scale.

The Real Partnership

The best AI systems will not remove humans from important work.

They will remove avoidable friction around human judgment.

They will summarise the case, surface the anomaly, draft the response, find the pattern, prepare the evidence, and make the decision easier to inspect.

Then the human decides where judgment, accountability, ethics, or regulation demands it.

That is the human-AI partnership worth building.

In the next post, we will look at how to assess where your organisation currently stands in its AI journey and what to build next.

References

- Bank Info Security: The AI Wave in Payments Industry

- Swift: Harnessing AI in the Fight Against Payments Fraud

- OWASP Top 10 for LLM Applications

- AWS Well-Architected Framework

Written by Haris Habib from Sydney, Australia | December 2025 This is the second post in a multi-part series on AI adoption.