Australia is a better startup market than it often gives itself credit for.

But not because it is a miniature version of Silicon Valley.

The best startup opportunities in Australia are the problems this country feels early, sharply, and with enough consequence that solving them here can become an advantage elsewhere.

Distance.

Labour scarcity.

Critical infrastructure.

Harsh operating environments.

Regulated industries.

Energy transition.

Sovereign capability.

Those are not only national constraints. For founders, they are unusually good product discovery environments.

The 2026 Signal

The market is already telling us where attention is moving.

| Signal | What it means for founders |

|---|---|

| Cut Through’s 1Q 2026 report recorded $1.8 billion in announced funding across 81 venture rounds and 26 accelerator rounds. | The formation engine is active again. |

| AI-first and AI-enabled companies accounted for more than half of Q1 deals. | AI is no longer a niche sector. It is becoming a layer across many sectors. |

| Several of the quarter’s largest rounds were in space and defence, hardware, robotics, sensors, cybersecurity, digital identity, life sciences, biotech, climate, and energy. | Capital is moving beyond traditional SaaS into harder, more strategic systems. |

| The National Reconstruction Fund Corporation is investing across seven priority areas including renewables, medical science, defence capability, transport, and enabling capabilities. | Policy is also leaning toward strategic industrial capability, not only software convenience. |

| In the 2026 Tech Leaders Survey, 78% of leaders named AI as the defining trend for 2026, but only 7% said Australia was ready for future AI demand to a great extent. | Demand is arriving faster than capability. That gap is an opportunity. |

This is the useful reading of the market: Australia’s next good startups are less likely to be “X for Australia” and more likely to be companies that turn an Australian constraint into exportable know-how.

The Opportunity Rule

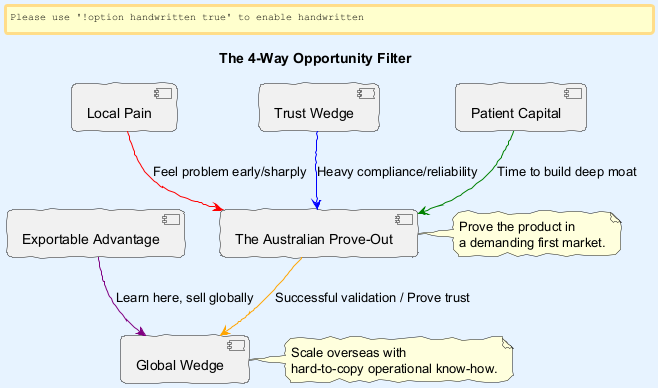

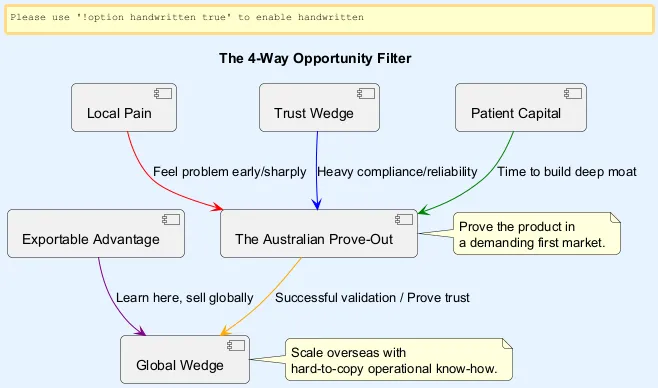

The strongest opportunities usually sit at the overlap of four things:

| Ingredient | The founder question |

|---|---|

| Local pain | Does Australia feel this problem intensely enough to become an excellent first market? |

| Exportable advantage | If we solve it here, does the learning travel to other markets? |

| Trust wedge | Is there a hard requirement around safety, regulation, reliability, or sovereignty that weak competitors will struggle to meet? |

| Patient capital | Is there a path to build something defensible before the market demands easy software margins? |

That filter matters because Australia is not large enough to support many “local-only” venture outcomes.

But it is large enough, difficult enough, and sophisticated enough to be a first market for globally relevant products.

Six Opportunity Zones Worth Taking Seriously

These are not the only opportunities in Australia.

They are the areas where current market signals, national priorities, and real operating pain line up especially well.

| Opportunity zone | Why Australia is a good first market | Founder wedge |

|---|---|---|

| AI for regulated and operational work | Banks, insurers, healthcare, government, mining, utilities, and infrastructure operators all need productivity gains without losing control. | AI systems with workflow evidence, human approval, audit trails, and measurable business outcomes. |

| Grid, storage, and industrial decarbonisation | Australia’s energy transition is forcing new coordination across generation, storage, transmission, and customer-owned assets. The draft 2026 Integrated System Plan points to very large long-term investment needs across the grid. | Forecasting, orchestration, inspection, asset intelligence, energy optimisation, and industrial efficiency products. |

| Defence, autonomy, and sensing | The 2026 National Defence Strategy and Defence’s sovereign industrial priorities put more emphasis on autonomous systems, battlespace awareness, test and evaluation, and sovereign industrial resilience. | Dual-use autonomy, navigation, simulation, sensing, assurance, and maintenance systems. |

| Health, diagnostics, and care operations | Australia has strong clinical research, a demanding health system, and policy interest in medical science capability. The Medical Science Co-investment Plan explicitly points to AI, machine learning, and biomedical technology as market opportunities. | Diagnostics, clinician workflow, hospital operations, medtech manufacturing, and AI with real clinical governance. |

| Cybersecurity, identity, and sovereign digital infrastructure | Trust is now a product requirement, not a feature request. The NRFC has already framed sovereign cloud and cybersecurity as national capability concerns. | Digital identity, compliance automation, secure infrastructure, fraud prevention, and audit-ready cyber products. |

| Resources, agriculture, and climate adaptation | Australia has world-class mining, agriculture, water stress, extreme weather, and long supply chains. Those conditions create painful, measurable problems earlier than many markets. | Robotics, remote operations, traceability, water efficiency, predictive maintenance, and climate-resilience tools. |

The pattern is not “deep tech good, software bad.”

The pattern is that the best opportunities are attached to expensive, consequential workflows where Australia already has a reason to care.

Why These Markets Are Better Than They Look

At first glance, many of these sectors seem harder than building another workflow app.

They are.

That is exactly why they are interesting.

Easy products attract many entrants.

Hard products create fewer serious competitors, stronger customer stickiness, and deeper learning loops when the founding team has real domain access.

| Australian constraint | Startup upside |

|---|---|

| Remote operations | Better automation, sensing, and fleet management products. |

| Expensive labour | Stronger ROI for productivity and robotics tools. |

| Critical infrastructure | Buyers care about reliability, resilience, and evidence. |

| Harsh climate | Climate adaptation can be tested against real operating stress. |

| Regulated markets | Trust becomes a moat when the product is designed properly. |

| Small domestic market | Founders are forced to think globally earlier. |

The local market does not need to be the final market.

It needs to be a credible proving ground.

What I Would Be Careful About

Not every “Australian opportunity” is a good startup opportunity.

| Weak shape | Why it disappoints |

|---|---|

| A US SaaS clone with an Australian flag on it | The market is smaller and the differentiation is thin. |

| A shallow AI wrapper with no workflow ownership | Models commoditise quickly; distribution and trust do not. |

| A grant-shaped company with no real buyer | Funding can start a project, but only customers validate a company. |

| A regulated product that treats security and governance as later work | Enterprise buyers discover the gap before scale arrives. |

| A hardware story with no service, data, or software compounding loop | The business becomes capital heavy without enough learning advantage. |

Australia is a good place to build difficult companies.

It is a less forgiving place to build vague ones.

The Security And Well-Architected Gap

This matters more in the Australian opportunity set because so many of the best markets are trust-heavy.

If the product touches health data, industrial controls, defence workflows, identity, money movement, or critical infrastructure, “we will harden it later” is not a serious scale-up plan.

| Trust question | Weak version | Strong version |

|---|---|---|

| Can the system protect sensitive data? | Security appears in the enterprise questionnaire stage. | Data classification, access control, encryption, retention, and incident response are designed from the start. |

| Can it keep working when conditions degrade? | A pilot works in a happy-path demo. | SLOs, observability, fallback modes, runbooks, and tested recovery are part of the product. |

| Can buyers understand what happened? | AI or automation outputs are difficult to reconstruct. | Decision traces, evidence, approvals, and audit logs are retained. |

| Can it scale economically? | Compute, cloud, or hardware costs are vague. | Cost drivers, budgets, routing, and unit economics are visible early. |

| Can the company survive procurement? | Security, compliance, and reliability evidence is assembled reactively. | Trust evidence is productised alongside the customer experience. |

This is where the AWS and Google Cloud Well-Architected frameworks are useful even for young companies: not as paperwork, but as a reminder that security, reliability, performance, cost, and operational excellence become part of the product in strategic markets.

The Founder Filter

If I were testing a startup idea in Australia now, I would ask seven questions:

- Does Australia feel this pain earlier or more intensely than other markets?

- Does solving it here create knowledge, data, workflow access, or trust that travels?

- Is there a real buyer with budget, not only an interested stakeholder?

- Can the founding team access the workflow deeply enough to learn faster than outsiders?

- Does the solution become more valuable as it becomes safer, more reliable, and more auditable?

- Is there a plausible capital path for the kind of company this really is?

- After the first Australian customers, is the global wedge obvious?

If the answer is yes across most of those questions, the idea is worth serious attention.

If the only strong answer is “the market is growing,” keep looking.

The Real Australian Opportunity

The most interesting Australian startups over the next decade will probably not look like local copies of American winners.

They will look like companies born from problems this country understands unusually well:

- how to operate across distance

- how to automate expensive work

- how to harden critical systems

- how to build trust in regulated environments

- how to manage energy, infrastructure, health, defence, and resources under real constraints

That is the better mental model.

Australia’s best startup opportunities are not small markets.

They are first markets.

The next question is whether Australia can help the best of those companies keep scaling from here once they become important. I wrote about that next-stage challenge in Australia’s Company-Formation Drain.

Sources and Further Reading

- Cut Through Quarterly 1Q 2026

- Tech Council of Australia and Datacom: Tech Leaders Survey 2026

- National Reconstruction Fund Corporation priority areas

- NRFC: Understanding the Enabling Capabilities Priority Area

- AEMO: Draft 2026 Integrated System Plan

- 2026 National Defence Strategy and Integrated Investment Program

- Sovereign Defence Industrial Priorities

- Medical Science Co-investment Plan

- AWS Well-Architected Framework

- Google Cloud Well-Architected Framework

Written by Haris Habib from Sydney, Australia | May 2026