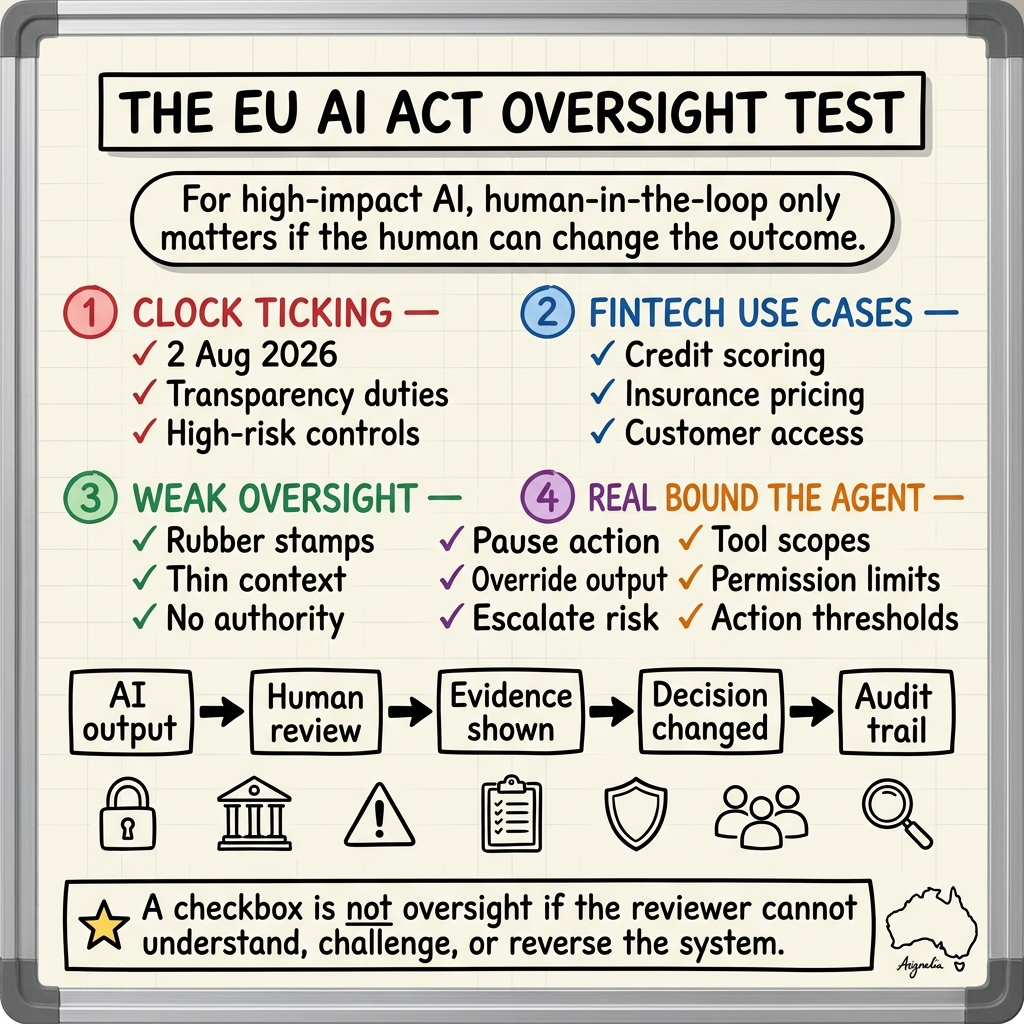

The EU AI Act’s next major application date is close enough that fintech leaders should stop treating it as a distant European policy story.

From 2 August 2026, the AI Act becomes broadly applicable, with several important exceptions and transition rules. The Commission also says transparency obligations will come into effect in August 2026, including requirements to inform people when they interact with AI systems or are exposed to certain AI-generated or manipulated content. (European Commission, European Commission)

For fintechs, the headline is not simply “Europe has an AI law.”

The sharper question is this:

Is your human-in-the-loop control actually oversight, or is it just a checkbox?

That distinction matters because many fintech use cases sit close to high-impact decisions: creditworthiness, insurance pricing, onboarding, fraud intervention, complaints, collections, and access to essential financial services.

Why fintech should pay attention

The AI Act classifies some financial-services use cases as high-risk. The Regulation specifically refers to AI systems used to evaluate the creditworthiness of natural persons or establish a credit score, with an exception for systems used to detect financial fraud. It also refers to AI systems used for risk assessment and pricing in life and health insurance. (EUR-Lex)

That matters because high-risk AI systems are not governed by vibes. They require discipline around risk management, data governance, technical documentation, logging, transparency, human oversight, robustness, accuracy, and cybersecurity.

Some obligations have staggered timing, and the Commission has noted simplification and transition issues for certain high-risk systems embedded in regulated products. But that nuance should not lead fintechs to relax. The direction is already clear: if an AI system influences a consequential decision about a person, the market will expect stronger evidence, stronger controls, and clearer accountability.

That is exactly where agentic AI makes the question more urgent.

The danger of fake human oversight

Most organisations can claim there is a human somewhere in the workflow.

That is not enough.

A real human-in-the-loop design gives a person enough information, time, authority, and interface control to intervene meaningfully. A checkbox version merely routes an AI-generated recommendation past a human who is too overloaded, too under-informed, or too constrained to challenge it.

The difference looks like this:

| Checkbox oversight | Real oversight |

|---|---|

| Human clicks approve after the model acts | Human can stop, override, or escalate before action |

| Reviewer sees only a recommendation | Reviewer sees evidence, confidence, limits, and alternatives |

| Exceptions are buried in queues | Exceptions are prioritised by risk and customer impact |

| Logs exist somewhere technical | Logs support audit, investigation, and remediation |

| Oversight is designed after the model | Oversight is part of the workflow architecture |

This is not a philosophical distinction. It is a product design distinction.

Article 14 is a design problem, not just a legal clause

The AI Act’s Article 14 addresses human oversight for high-risk AI systems. It says high-risk systems must be designed and developed in a way, including appropriate human-machine interface tools, that allows effective oversight by natural persons. The purpose is to prevent or minimise risks to health, safety, or fundamental rights. (EUR-Lex)

For product leaders, this translates into concrete design questions:

- Can a human understand why the system recommended an action?

- Can they see the data and assumptions that mattered?

- Can they detect when the system is outside its competence?

- Can they override or stop the action?

- Can they avoid automation bias rather than simply rubber-stamping the output?

- Can the organisation later reconstruct what happened?

If the answer is no, the system may have a human in the process, but not meaningful human oversight.

The agentic AI version is harder

Traditional AI systems often recommend. Agentic systems can act.

That changes the risk model.

A customer-service classifier might route an email. An agent might draft the response, access account data, trigger a refund, place a hold, or escalate a fraud case. Each additional action expands the oversight problem.

The governance question becomes:

What decisions are we willing to delegate, under what constraints, and how do we reverse them?

That question should sit at the centre of every fintech agent deployment.

A safe agentic workflow should have:

- bounded permissions,

- clear action thresholds,

- human approval for high-impact steps,

- audit logs that capture tool use and reasoning context,

- incident review when outputs are wrong,

- and a kill switch or pause mechanism when behaviour drifts.

The point is not to remove autonomy. The point is to make autonomy governable.

What fintechs should do before August

The best response is not a last-minute policy document. It is a practical oversight review.

Start with five moves.

1. Inventory AI systems by decision impact

Do not start with model names. Start with customer impact.

Which workflows affect access to money, credit, insurance, onboarding, fraud outcomes, fees, collections, disputes, or complaints? Which of those workflows use AI, machine learning, rules engines, or agentic automation?

2. Classify human oversight honestly

For each workflow, identify whether the human is:

- informed after the fact,

- approving a recommendation,

- reviewing exceptions,

- supervising live action,

- or empowered to stop the system.

Those are different control models.

3. Test for automation bias

If humans approve 99% of recommendations because the interface makes disagreement hard, you may not have oversight. You may have ceremony.

Measure override rates, escalation quality, queue pressure, review time, and whether reviewers understand model limitations.

4. Make logs useful to humans, not just systems

Record-keeping matters, but a log that only engineers can interpret may not support compliance, dispute resolution, or customer remediation. The audit trail should help a future reviewer understand what happened, why it happened, who approved it, and how it was corrected.

5. Design reversal into the workflow

If an AI system can block, reject, freeze, price, prioritise, or escalate, the organisation needs a safe way to pause, override, explain, and recover.

In regulated markets, reversibility is not a nice-to-have. It is part of trust.

The commercial point

A lot of AI teams still talk about human-in-the-loop as if it is a temporary compromise before full autonomy.

That is too simplistic for fintech.

In regulated financial services, meaningful human oversight may be one of the features that allows more automation to be adopted. It gives buyers, customers, boards, and regulators confidence that the system can be trusted with higher-impact workflows.

That means the winners will not be the companies that claim the least human involvement. They will be the companies that know exactly where humans still matter and design those moments properly.

As the EU AI Act’s August 2026 application date approaches, the practical test is simple:

If your human-in-the-loop control cannot change the outcome, it is probably not oversight. It is theatre.