Australia is running a world-class incubator for future US companies.

That sounds harsh.

It is also becoming harder to ignore.

The early-stage story is genuinely strong. Australia is producing more ambitious AI, robotics, space, infrastructure, defence, cyber, climate, and health technology companies than it often gives itself credit for. In Cut Through’s 1Q 2026 Australian startup funding report, AI-first and AI-enabled companies accounted for more than half of Q1 deals. The same report showed $1.8 billion in announced startup funding across 81 venture rounds and 26 accelerator rounds, Australia’s strongest first-quarter result since the 2022 peak.

But the headline is not the whole story.

The structure underneath is more important.

| Signal | What the data says | Why it matters |

|---|---|---|

| Funding recovered | Q1 2026 recorded $1.8 billion across 81 venture rounds and 26 accelerator rounds. | Australia is still forming venture-backed companies at serious volume. |

| Capital concentrated | The top 20 deals captured 79% of Q1 capital. | The market is open, but only for companies that clear a much higher conviction bar. |

| Smaller rounds thinned | Sub-$10 million rounds contributed their lowest share of capital in five years across Q4 2025 and Q1 2026. | The middle of the funding ladder is becoming less forgiving. |

| Series B takes longer | Median company age at Series B reached 9.7 years. | The journey from promising startup to scaled company is stretching. |

| The path has slowed | The path from Pre-Seed to Series B has nearly tripled in length since 2021. | The scale-up phase is now the real ecosystem test. |

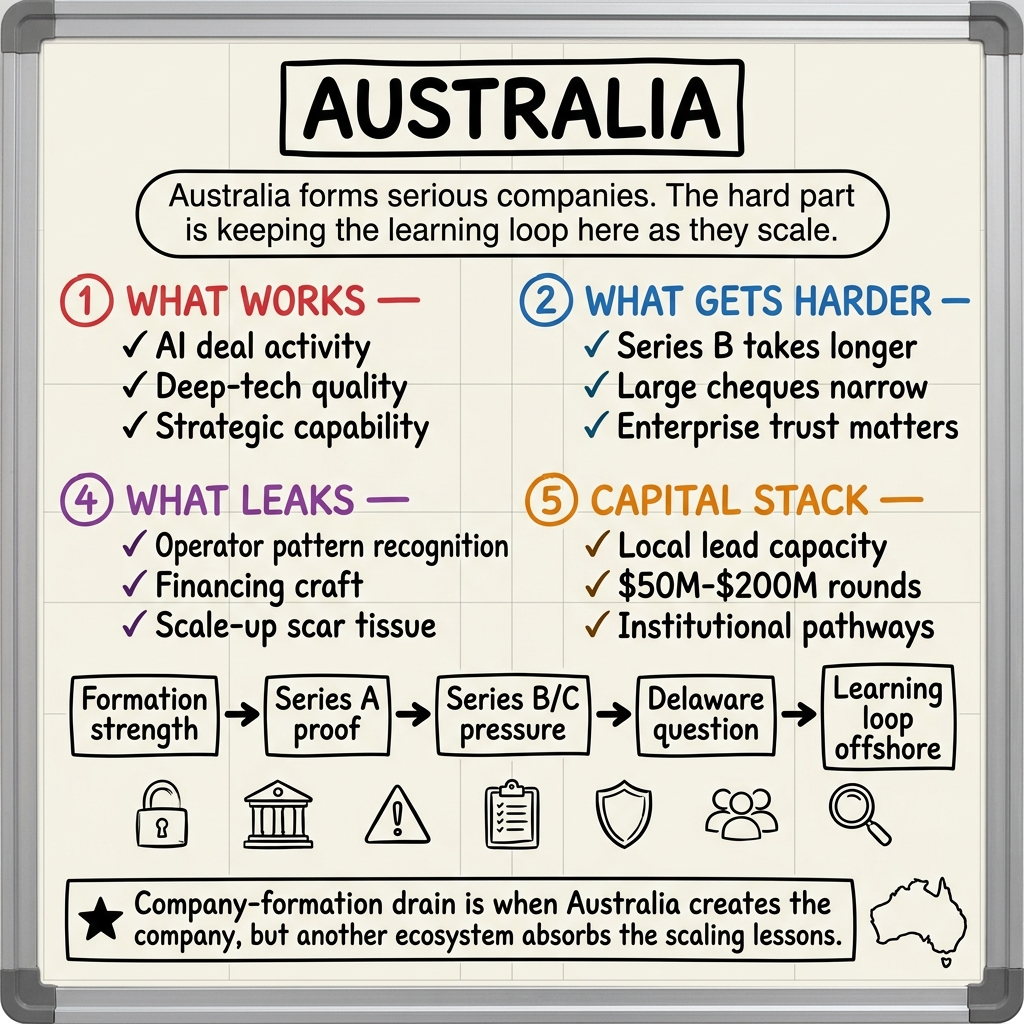

This is the important shift: Australia is not failing at startup formation.

Australia is failing to make enough of its most important companies grow up here.

The Difference Between Formation And Scale

An incubator is where companies are born.

An ecosystem is where they grow up.

Australia is increasingly good at the first part. We have technical universities, strong cloud and software talent, applied industry problems, trusted institutions, research capability, credible early-stage funds, and a founder culture that is becoming more globally fluent.

That is why the new cohort matters.

| Company | What it is building | Why it matters strategically |

|---|---|---|

| Advanced Navigation | Assured positioning, navigation, autonomy, and sensing technology for air, land, sea, defence, and industrial systems. | Navigation and autonomy are core infrastructure for defence, robotics, logistics, maritime, aerospace, and critical industry. |

| Neara | Physics-enabled digital twins for utilities and infrastructure operators. | Grid resilience, energy transition, asset modelling, and infrastructure planning are national capability questions. |

| Gilmour Space | Integrated launch vehicle, satellite platform, and spaceport capability from Australia. | Sovereign launch and space manufacturing capability shape defence, communications, Earth observation, and industrial resilience. |

These are not lightweight SaaS experiments.

They are strategic capability companies.

That is why the question matters.

The national test is not whether Australia can create promising startups. We can.

The test is whether Australia can help the most important ones scale without slowly handing their centre of gravity to another ecosystem.

The Scale-Up Gravity Problem

Seed funding is important, but seed is no longer the real proof of ecosystem strength for strategic AI and deep-tech companies.

The harder proof arrives later.

At seed, a company can often move with a small technical team, founder intensity, early pilots, cloud credits, research relationships, and a sharp customer wedge.

At Series A, it starts proving product-market fit, repeatable sales motion, production readiness, and the first version of enterprise trust.

At Series B and C, the game changes.

The company is no longer only building a product. It is building an institution.

It needs growth capital, global sales leadership, enterprise procurement credibility, compute and infrastructure capacity, security and compliance depth, government or regulated-market trust, senior executives who have scaled before, and a balance sheet that makes large customers believe it will still be around in five years.

That is the layer Australia still does not produce consistently enough.

The problem is not that founders look overseas. They should. Global companies need global capital, global customers, and global ambition.

The problem is when looking overseas becomes the only credible path.

The Delaware Flip Is A Symptom

When Australian founders pursue US capital, the structure question often arrives quickly:

Are you a Delaware C-Corp?

That question is not irrational.

For some companies, especially those selling deeply into the US market, a Delaware structure can be commercially sensible. AirTree’s guide for Australian founders explains why US and international investors often prefer Delaware structures. Silicon Valley Bank also notes that Delaware incorporation is often expected by venture investors.

The problem is not the Delaware flip itself.

The problem is when the Delaware flip stops being a deliberate market-entry decision and becomes the default workaround for Australia’s missing growth-stage layer.

Because company structure is not just paperwork.

When the holding company moves, the centre of gravity moves with it.

| What moves | Why it matters |

|---|---|

| Cap table | The company’s future financing path starts orbiting another capital market. |

| Board expectations | Governance norms, risk appetite, and strategic priorities shift toward the lead market. |

| Senior hiring logic | The next CFO, CRO, general counsel, and independent directors are more likely to be hired offshore. |

| Customer trust | Enterprise and government buyers often follow the market where the company is validated. |

| Exit logic | Acquisition pathways, IPO expectations, and strategic partnerships become anchored elsewhere. |

| Ecosystem learning | The next generation loses exposure to the hardest scaling lessons. |

The engineering team may remain in Sydney, Melbourne, Brisbane, Perth, Adelaide, Canberra, or the Gold Coast for a while. The founders may still feel Australian. The product may still have been born from Australian problems.

But ownership, governance, financing, and exit pathways begin orbiting another system.

At one company, that can be a rational commercial decision.

Across an ecosystem, it becomes a leak.

This Is Not Just Brain Drain

“Brain drain” is too narrow.

Brain drain is when talented people leave.

Company-formation drain is when the learning loop leaves.

It is the loss of board pattern recognition, CFO muscle, late-stage financing craft, enterprise sales experience, procurement credibility, security and compliance maturity, acquisition playbooks, and scale-up scar tissue that teach the next generation how to build harder companies.

Those capabilities are not created by speeches, grants, or strategy decks. They are created by repeated exposure to companies under pressure.

That is the quiet problem.

If Australia’s most important AI and deep-tech companies repeatedly go offshore at the hard stage, Australia does not only lose some ownership upside. It loses the chance to train the operators, directors, investors, and future founders who would make the next company easier to scale from here.

Why AI Makes This More Strategic

This would matter in any technology wave.

It matters more in AI because AI is becoming a general-purpose capability layer across the economy.

The Tech Council of Australia and Datacom’s 2026 Tech Leaders Survey found that 78% of Australian tech leaders identify AI and machine learning as the defining trend for 2026, while only 7% believe Australia currently has the capability and infrastructure to meet future AI demand to a great extent.

That gap is the whole issue.

Australia has demand. Australia has founders. Australia has applied industry problems. Australia has early company formation.

But if the best AI and deep-tech companies are structurally pulled offshore at the growth stage, Australia risks becoming a talent and idea supplier rather than a durable owner of strategic technology.

Meanwhile, the US capital market has enormous gravitational pull. KPMG’s Q1 2026 Venture Pulse reported record global venture investment of $330.9 billion in Q1 2026, with the US alone accounting for $267.2 billion of the Americas total and AI megadeals driving the surge.

Australia cannot match that dollar for dollar.

It does not need to.

But it does need enough growth-stage credibility to give its best companies a real choice.

The Practical Centre-Of-Gravity Test

The better question is not:

Did the company go overseas?

Great companies should sell globally, hire globally, raise globally, and compete globally. If the US is the right market, founders should go hard at the US. If a Delaware structure is the right commercial move, founders should understand it and make the decision deliberately.

The better question is:

Can a global AI or deep-tech company stay meaningfully Australian while it scales?

Meaningfully Australian does not mean parochial.

It means enough of the company’s compounding machinery remains here.

| Centre-of-gravity test | What “meaningfully Australian” looks like |

|---|---|

| Decision-making | Important strategic decisions are still made by leaders with a serious Australian base. |

| Technical capability | Senior engineering, product, research, manufacturing, or infrastructure capability remains here. |

| Governance learning | Australian directors and executives are exposed to real scale-up decisions. |

| Customer formation | Australian government and enterprise buyers become credible early reference customers. |

| Capital participation | Local investors can participate meaningfully beyond seed and Series A. |

| Talent flywheel | People trained inside the scale-up become the next founders, operators, and board members. |

If those things stay here often enough, the ecosystem compounds.

If they move offshore by default, Australia keeps the origin story while another system captures the learning.

What Australia Should Build Next

The answer is not protectionism.

The answer is a stronger scale-up layer.

| Layer | What Australia needs | Why it matters |

|---|---|---|

| Growth capital | Local investors and co-investment vehicles that can credibly lead or co-lead $50 million to $200 million rounds. | Strategic companies need enough domestic capital to avoid offshore structure becoming the only viable path. |

| Institutional pathways | Professionally managed superannuation and institutional exposure to local venture growth. | Australia has deep pools of capital, but too little of it reaches strategic private technology companies. |

| First customers | Government procurement and corporate buying that can validate Australian technology earlier. | Grants help companies start; serious customers help them grow. |

| Operator bench | More CFOs, CROs, security leaders, enterprise sales leaders, and chairs who have scaled global technology companies. | Capital alone is not enough if the company cannot build trust, governance, and execution muscle. |

| Compute and infrastructure | Better access to AI infrastructure, cloud partnerships, data capability, and secure deployment environments. | AI and deep-tech companies are capital intensive because infrastructure is part of the product. |

| Strategic procurement | Clearer pathways for defence, energy, health, infrastructure, and government buyers to work with local scale-ups. | Sovereign capability is not built only through policy. It is built when demanding customers buy early enough. |

It also needs security and Well-Architected maturity to become part of the scale-up muscle, not something founders bolt on after the first enterprise customer asks for it.

| Gap | Why it matters at Series B and C |

|---|---|

| Security maturity | Defence, infrastructure, finance, health, and government customers need evidence of secure design, access control, incident response, and data protection. |

| Operational excellence | Large customers need confidence that the company can support production systems, not only build impressive technology. |

| Reliability engineering | Strategic capability companies need tested recovery, observability, runbooks, and service-level discipline. |

| Cost and performance discipline | AI and deep-tech companies can burn capital through compute, infrastructure, and inefficient scaling patterns. |

| Governance evidence | Boards and buyers need proof of ownership, risk management, auditability, and decision quality. |

If Australia wants more companies to scale from here, it needs more than capital. It needs the local operator bench that can help founders pass the enterprise trust test earlier.

None of this requires pretending every startup is a national champion.

Most will not be.

But the few that are strategically important should not face only two options: stay undercapitalised or become foreign-centred before they scale.

What A 10-Star Ecosystem Would Feel Like

A 5-star ecosystem lets founders start companies.

A 7-star ecosystem helps the best companies raise, sell, hire, and govern with less friction.

A 10-star ecosystem does something more powerful: it makes the founder feel that staying meaningfully Australian improves the company’s odds of becoming globally important.

That would mean:

- A Series B quality founder can find local investors who understand the category and can write serious cheques.

- A government or enterprise buyer can become a demanding first customer without forcing the startup through a maze built for incumbents.

- A board can be assembled in Australia with people who have seen the movie before.

- A company can raise internationally without automatically moving its centre of gravity offshore.

- Early employees can see a path from Australian scale-up experience to future founder, executive, investor, or director roles.

- Global customers see the Australian base as a signal of capability, trust, resilience, and technical depth.

That is the standard.

Not isolation.

Not nationalism for its own sake.

An ecosystem that compounds.

The Practical Test For The Next Decade

Here is the test I would use.

When an Australian AI or deep-tech company reaches Series B quality, can it raise a globally competitive round while keeping Australia as a meaningful centre of ownership, decision-making, capability, and talent?

Can it win serious first customers here?

Can it build a board here that customers and global investors respect?

Can it hire senior operators here who have already lived the scale-up journey?

Can it go global without making Australia only the birthplace?

If the answer is yes often enough, the ecosystem compounds.

If the answer is no, Australia will keep celebrating seed rounds while quietly exporting the companies that matter most.

The point is not to trap companies here.

The point is to make staying meaningfully Australian a competitive advantage, not a constraint.

That is the difference between an incubator and an ecosystem.

An incubator is where companies are born.

An ecosystem is where they grow up.

Australia is very good at the first part.

The next national technology challenge is the second.

Sources and Further Reading

- Cut Through Quarterly 1Q 2026

- State of Australian Startup Funding 2025

- Tech Council of Australia and Datacom: Tech Leaders Survey 2026

- KPMG Venture Pulse Q1 2026

- Advanced Navigation: Industries

- Neara: Physics-enabled digital twin for utilities

- Gilmour Space Technologies

- AirTree: What Aussie startups need to know about the Delaware Flip

- Silicon Valley Bank: Why incorporate in Delaware?

- AWS Well-Architected Framework

- Google Cloud Well-Architected Framework

Written by Haris Habib from Sydney, Australia | May 2026