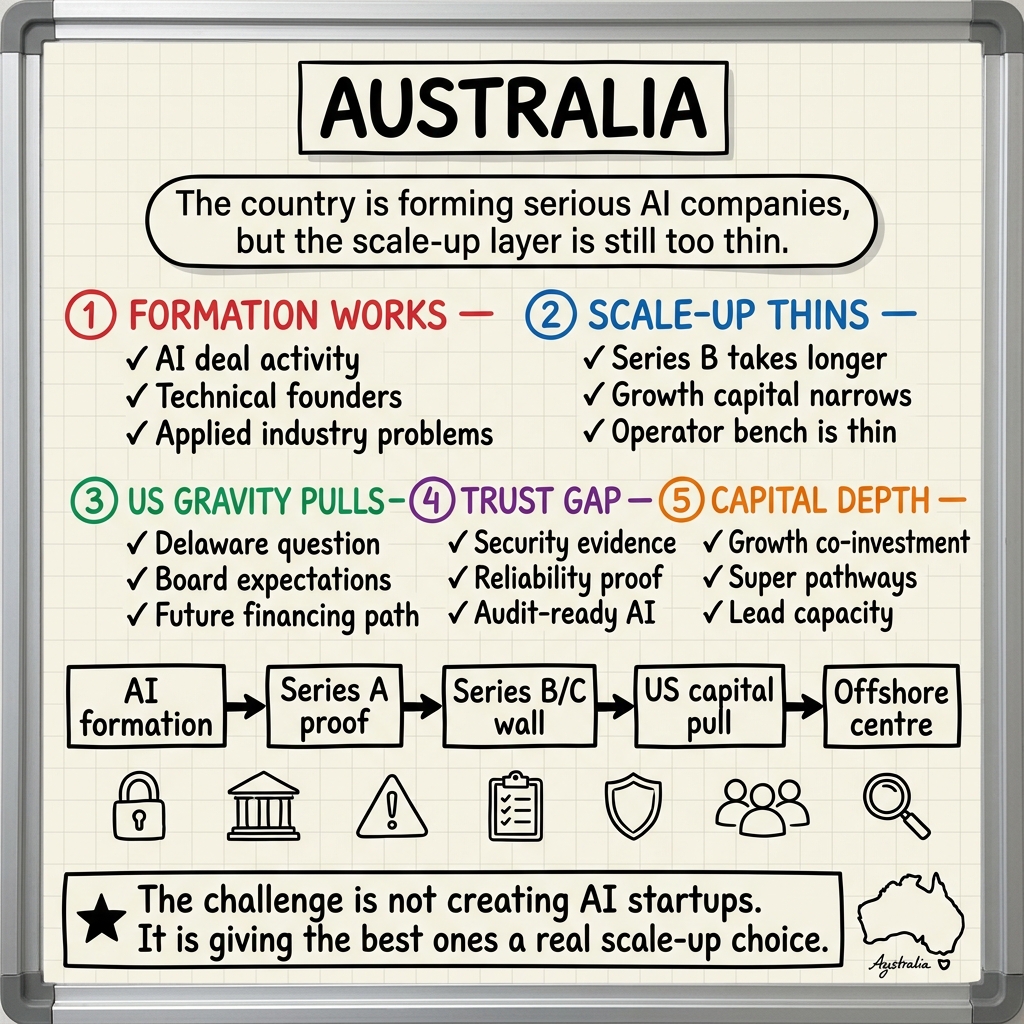

Australia is running a world-class incubator for future US companies.

That is the uncomfortable version of a mostly good-news story.

The good news is that Australia’s AI startup formation engine is working. AI is no longer a side theme in Australian venture. In Cut Through’s 1Q 2026 funding report, AI-first and AI-enabled companies accounted for more than half of Q1 deals. The same quarter recorded $1.8 billion in announced startup funding across 81 venture rounds and 26 accelerator rounds.

That is serious activity.

The bad news is that the system still thins out when the best companies need to scale.

The Market Signal

The useful signal is not only how much capital was raised. It is where the capital concentrated and how long the scale-up path has become.

| Signal | What it suggests |

|---|---|

| AI-first and AI-enabled companies made up more than half of Q1 deal activity. | Australia is forming AI companies at real pace. |

| The top 10 deals accounted for almost 60% of capital raised. | Capital is available, but concentrated around fewer high-conviction companies. |

| Sub-$10 million rounds contributed their lowest share of capital in five years across Q4 2025 and Q1 2026. | The early-to-middle funding ladder is less forgiving. |

| Median company age reached 6.7 years at Series A and 9.7 years at Series B. | The journey from formation to growth stage is taking longer. |

| The path from Pre-Seed to Series B has nearly tripled since 2021. | The scale-up phase is now the real bottleneck. |

That is not a simple “funding is down” story.

It is a maturity story.

Australia can form companies. The harder question is whether it can help the best ones become globally important while keeping a meaningful Australian centre of gravity.

Why AI Makes The Question Bigger

AI is not just another software category.

It is becoming an infrastructure layer for defence, health, energy, financial services, industrial systems, education, cyber, and government operations.

That changes the stakes.

If Australia’s most capable AI companies are structurally encouraged to become US-centred companies at the growth stage, Australia risks becoming a supplier of talent, ideas, and early technical validation rather than a durable owner of strategic capability.

This does not mean every AI startup should remain locally owned forever.

It means the country needs enough growth-stage depth that founders have a real choice.

The Series B/C Wall

For an AI company, the expensive part often begins after the product starts working.

At seed, a small technical team can use foundation-model APIs, cloud credits, open-source tooling, research relationships, and founder intensity to prove a wedge.

At Series A, the company starts proving repeatability: product-market fit, sales motion, implementation model, security posture, and early customer trust.

At Series B and C, the company needs a different machine.

| Scale-up requirement | Why it becomes hard |

|---|---|

| Growth capital | Larger rounds are needed for global sales, compute, hiring, and customer trust. |

| Enterprise credibility | Regulated and government buyers need proof the company will survive. |

| Compute and infrastructure | AI companies can carry heavier infrastructure costs than traditional SaaS. |

| Governance | Boards need experience with risk, compliance, global expansion, and capital strategy. |

| Senior operators | The company needs people who have scaled sales, finance, security, and operations before. |

| Global customer motion | The sales motion moves beyond founder-led pilots into repeatable enterprise adoption. |

This is where the Australian layer is still thin.

So founders do the rational thing.

They look outward.

Often to the US.

The Security And Well-Architected Gap

Growth-stage AI companies are not judged only on product ambition. They are judged on whether serious customers can trust them.

That means the scale-up gap is also a security and architecture gap.

| Scale-up trust question | What weak looks like | What strong looks like |

|---|---|---|

| Can the company protect sensitive data? | Security is handled as a late enterprise-sales checklist. | Data classification, access controls, encryption, audit, and incident response are designed early. |

| Can it pass enterprise procurement? | Security questionnaires trigger last-minute policy work. | SOC 2 or equivalent controls, vendor risk evidence, and clear operational ownership are ready. |

| Can it operate reliably? | The product works in pilots but lacks SLOs, monitoring, and recovery paths. | Reliability targets, dashboards, runbooks, and tested recovery are part of the product. |

| Can it scale economically? | Compute, model, and cloud costs are poorly understood. | Unit economics, cost budgets, model routing, and capacity planning are visible. |

| Can customers audit decisions? | AI outputs are hard to explain after the fact. | Decision traces, source evidence, approval paths, and governance records are retained. |

This is where Well-Architected thinking becomes more than a cloud checklist. For strategic AI companies, operational excellence, security, reliability, performance, and cost discipline are part of enterprise trust.

The Delaware Question

When Australian founders chase US capital, the structure question often arrives quickly:

Are you a Delaware C-Corp?

The question is not irrational. Silicon Valley Bank notes that Delaware incorporation is often expected by venture investors. AirTree’s guide for Australian founders explains why US and international investors often prefer Delaware companies.

For many companies, especially those selling deeply into the US, a Delaware flip can be commercially sensible.

The problem is when it becomes the default answer to Australia’s missing growth-stage layer.

When the holding company moves, the cap table, board expectations, future financing path, senior hiring logic, acquisition pathways, and tax upside can move with it.

At one company, that may be a rational choice.

Across an ecosystem, it becomes leakage.

What We Are Actually Exporting

The phrase “brain drain” is too narrow.

The risk is not only that individual engineers leave.

The risk is that Australia exports the company-building learning loop:

- directors who understand growth-stage AI governance

- CFOs who can finance compute-intensive companies

- enterprise sales leaders who can sell into regulated markets

- security and compliance leaders who can pass demanding customer reviews

- investors who have seen late-stage scaling pressure up close

- operators who become the next generation of founders

Those capabilities are created by repeated exposure to hard companies under pressure.

If the hardest stages mostly happen offshore, Australia’s next generation starts with less local pattern recognition.

What A Better Scale-Up Loop Looks Like

The answer is not isolation.

Great Australian companies should sell globally, hire globally, raise globally, and compete globally.

The better goal is to make Australia a place where global AI companies can remain meaningfully Australian while scaling internationally.

| Layer | What needs to improve |

|---|---|

| Growth capital | More local funds and co-investment vehicles that can lead or support large rounds. |

| Institutional capital | Clearer pathways for professionally managed superannuation exposure to venture growth. |

| First customers | Government and corporates buying strategically important local technology earlier. |

| Research commercialisation | More emphasis on company building, not only publication or licensing. |

| Operator talent | More repeat executives, CFOs, CROs, security leaders, and board members with scale-up experience. |

| Procurement trust | Faster pathways for credible startups to sell into regulated and public-sector buyers. |

None of this requires pretending every startup is a national champion.

Most are not.

But the few that are strategically important should not face only two choices: stay undercapitalised or become foreign-centred before they scale.

The Practical Test

Here is the test I would use.

When an Australian AI company reaches Series B quality, can it raise a globally competitive round while keeping Australia as a meaningful centre of ownership, decision-making, capability, and talent?

If the answer is yes often enough, the ecosystem compounds.

If the answer is no, Australia will keep celebrating seed announcements while quietly exporting the companies that matter most.

An incubator is where companies are born.

An ecosystem is where they grow up.

Australia is getting very good at the first part.

The next challenge is the second.

For a deeper version of this argument, see Australia’s Company-Formation Drain.

Sources and Further Reading

- Cut Through Quarterly 1Q 2026

- Tech Council of Australia and Datacom: Tech Leaders Survey 2026

- AirTree: What Aussie startups need to know about the Delaware Flip

- Silicon Valley Bank: Delaware incorporation

- KPMG Venture Pulse Q1 2026

- AWS Well-Architected Framework

- Google Cloud Well-Architected Framework

Written by Haris Habib from Sydney, Australia | May 2026