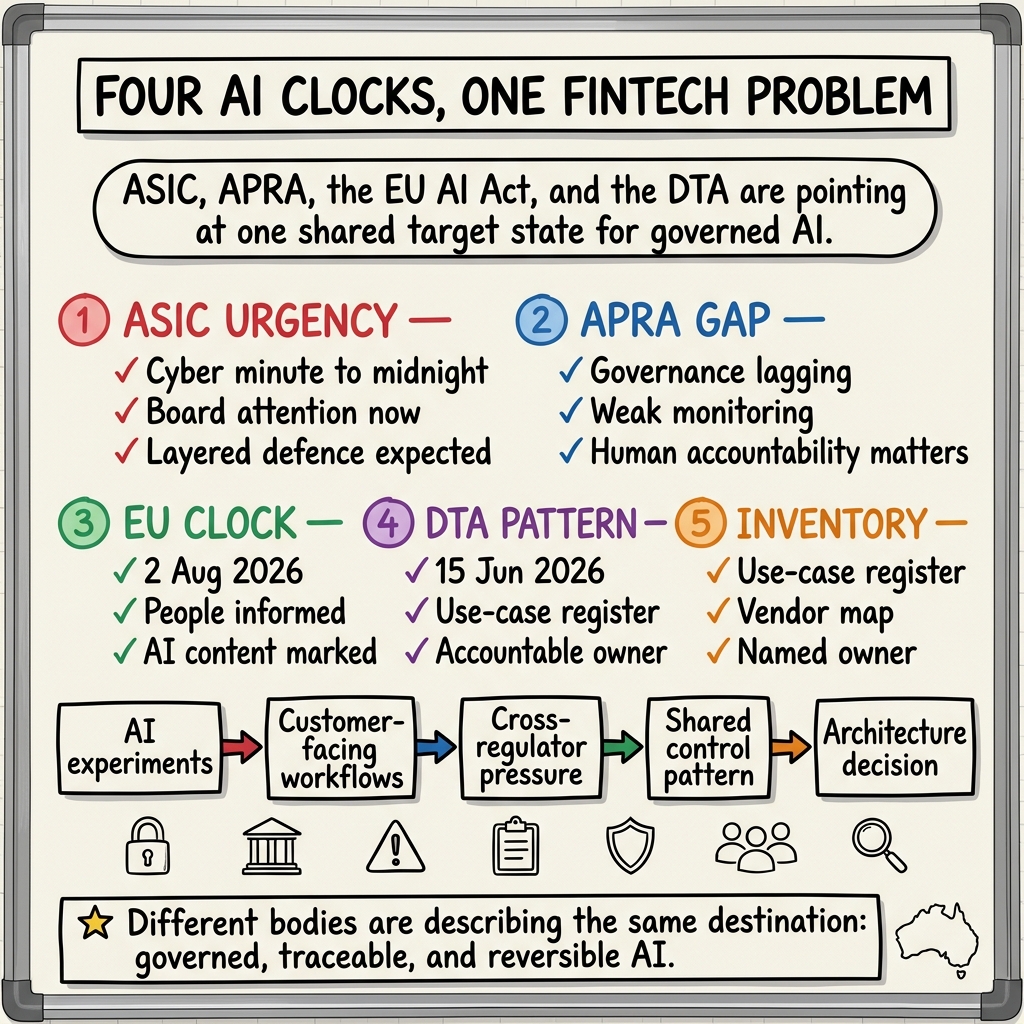

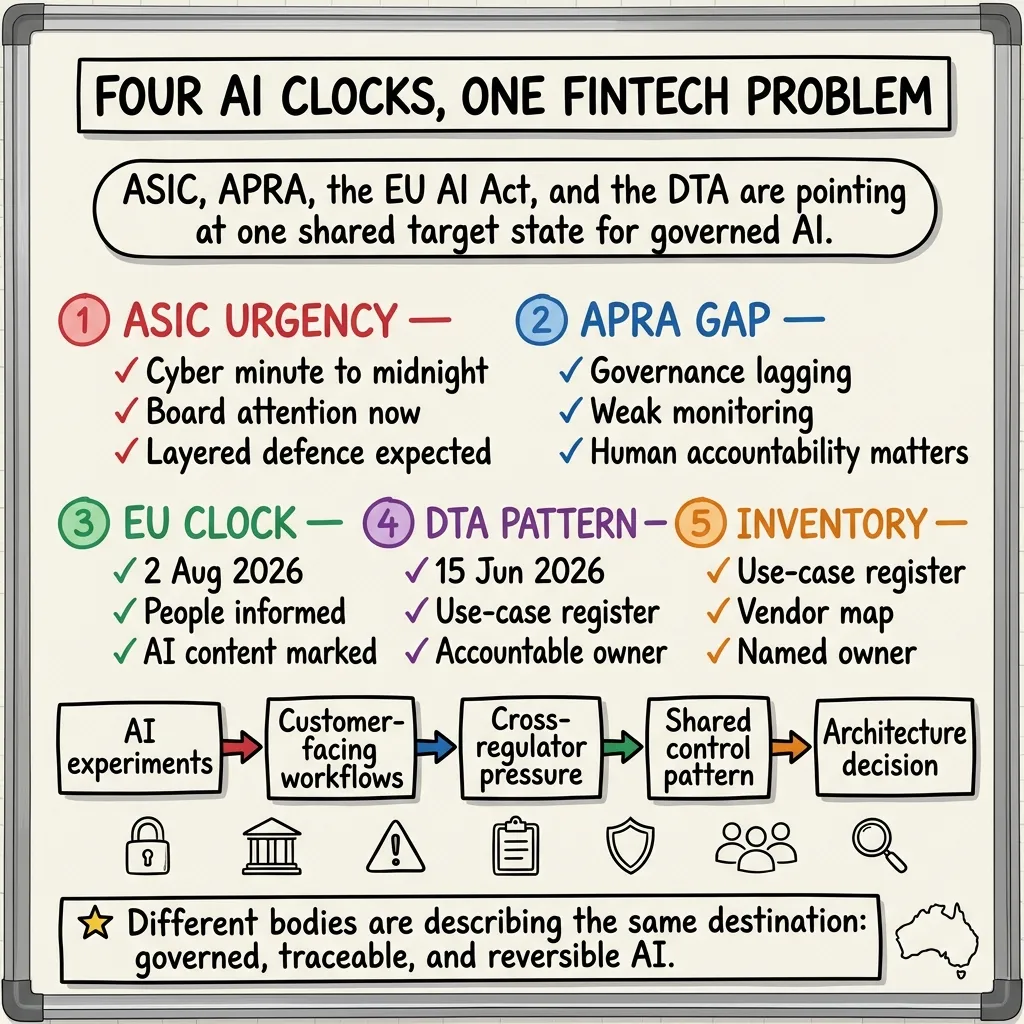

Four clocks.

ASIC says cyber is at “minute to midnight”.

APRA says AI governance is lagging adoption.

The EU AI Act transparency date is 72 days away.

The DTA’s first new mandatory AI governance requirement is 24 days away.

On Friday, 22 May 2026, those last two numbers are exact.

That does not mean Australian fintechs suddenly have four separate compliance programs to launch.

It means four different oversight bodies are converging on the same architecture question:

Can you show where AI is used, who owns it, how humans stay accountable, what customers are told, and how the system is recovered when something goes wrong?

That is the real AU fintech compliance stack now.

The four signals are different, but they rhyme

The trigger points are not identical.

ASIC is focused on cyber resilience. APRA is focused on prudential risk and governance maturity. The European Commission is focused on AI transparency obligations under the AI Act. The Digital Transformation Agency is setting mandatory governance patterns for Australian Government AI use.

But read the actual signals side by side and a common control model appears.

| Body | Current signal | What it means in practice |

|---|---|---|

| ASIC | On 8 May 2026, ASIC warned that cyber is at “a minute to midnight” and told entities to urgently strengthen cyber resilience as AI accelerates threats. Boards and executives are expected to act now. (ASIC) | Your AI stack cannot be separated from your cyber stack. |

| APRA | On 30 April 2026, APRA said AI adoption is accelerating, but governance has not matured at the same pace. It pointed to weak post-deployment monitoring, weak model behaviour monitoring, change management gaps, and a need for human involvement in high-risk decisions. (APRA) | AI governance has to be operational, not just policy-shaped. |

| EU AI Act | From 2 August 2026, people in the EU must be informed when they are interacting with AI systems or exposed to certain AI-generated or manipulated content. (European Commission, European Commission) | Customer-facing AI needs a disclosure layer, not just an internal approval memo. |

| DTA | The DTA says the first new mandatory requirement in the updated Policy for the responsible use of AI in government begins on 15 June 2026. Agencies must maintain an internal register of in-scope AI use cases, assign an accountable owner, and complete an AI impact assessment before deployment. (DTA) | The market is moving toward named use cases, named owners, and pre-deployment gates. |

The point is not that every Australian fintech is directly regulated by all four of those bodies in the same way.

The point is that all four are describing the same destination.

This is why it matters to fintechs now

Fintech sits at the intersection of regulated decisions, third-party dependency, customer trust, and fast-moving AI adoption.

That makes fragmented governance especially dangerous.

A fintech may have:

- a customer support copilot,

- a fraud triage model,

- onboarding automation,

- a decision support flow for disputes or hardship,

- AI in software engineering tooling,

- and vendor AI embedded inside platforms the business did not originally buy as “AI systems”.

Each of those creates a slightly different exposure pattern.

ASIC cares that the environment is resilient when attack speed, scale, and sophistication increase. APRA cares that governance, accountability, monitoring, and supplier risk are real in practice. The EU cares that people are informed when AI is part of the interaction. The DTA pattern matters because it is quickly becoming the cleanest public example of what procurement-grade AI governance looks like: register the use case, name the owner, assess the impact before go-live.

That is why the problem is architectural.

If your answer to each new AI obligation is a new spreadsheet, a new policy PDF, or a new committee deck, you are building compliance drag, not compliance capability.

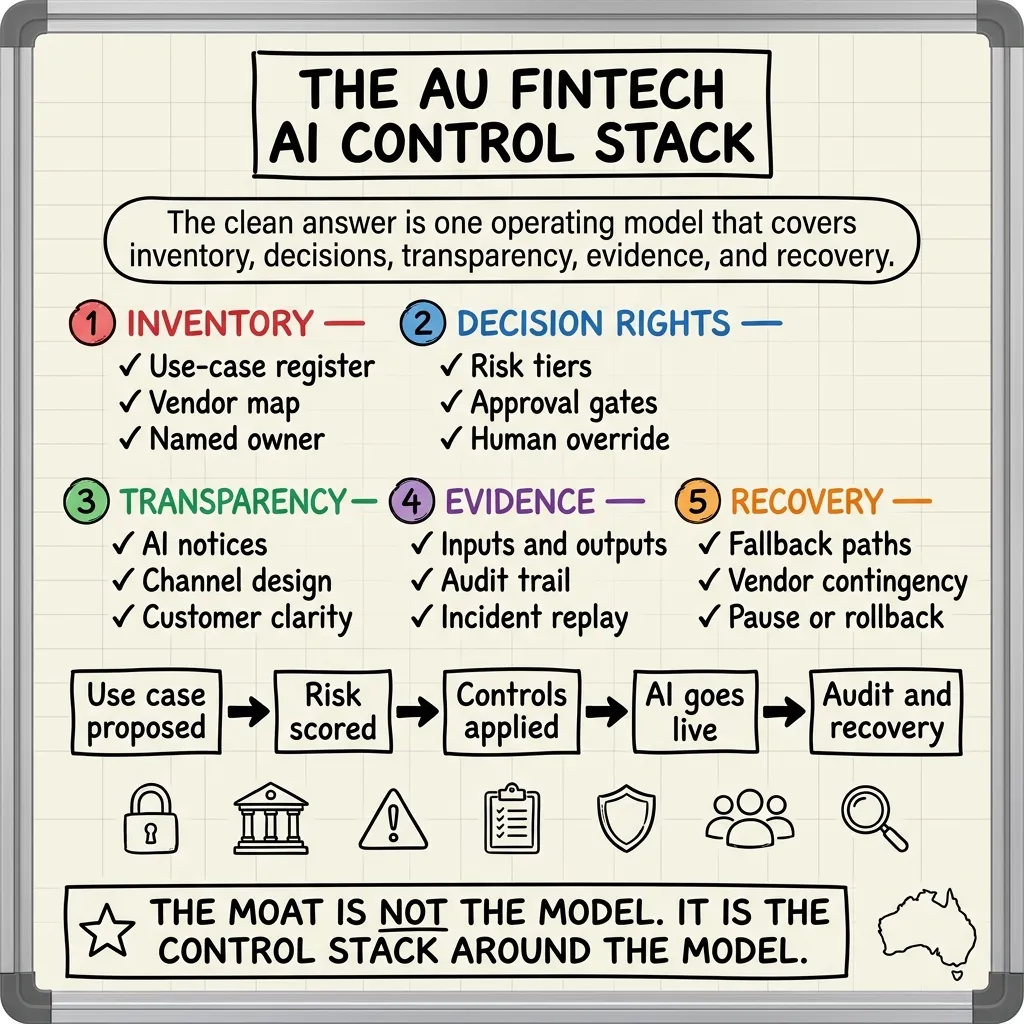

Most firms have four workstreams. They need one control stack.

The winning move is not to map each regulator to a separate project.

The winning move is to build one control stack that can satisfy multiple expectations at once.

Here is the shape of it.

1. Use-case inventory and ownership

You need a live inventory of AI use cases, models, vendors, embedded AI features, and workflow owners.

Not a one-off discovery exercise. A living system of record.

If someone asks:

- Where are we using AI?

- Which use cases are customer-facing?

- Which ones influence a consequential decision?

- Which vendor or model powers them?

- Who is accountable?

You should be able to answer in minutes, not after a two-week internal scavenger hunt.

This is the common thread between APRA’s lifecycle accountability expectations and the DTA’s use-case register plus accountable owner pattern.

2. Risk tiering and decision rights

Not every AI use case deserves the same control.

A summarisation assistant for internal notes is not the same as a workflow that influences onboarding, fraud escalation, credit decisions, pricing, disputes, or access to a service.

Each use case should have:

- a risk tier,

- a defined approval path,

- explicit decision rights,

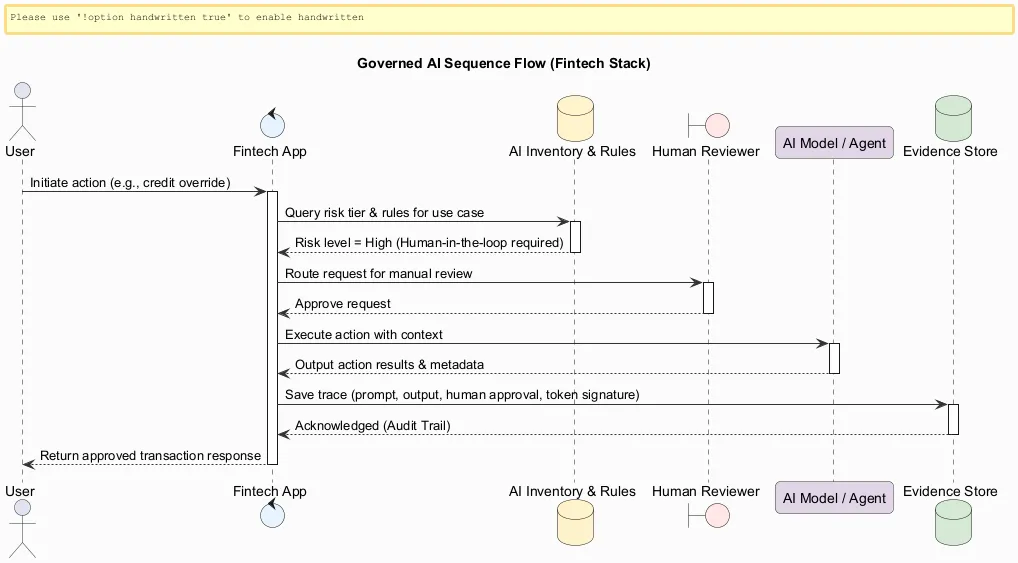

- and a rule for when a human must review, approve, or override.

This is where many teams still overestimate their maturity. They say there is a human in the loop, but cannot show what the human actually sees, when they see it, or whether they can change the outcome.

That is not meaningful oversight. It is ceremony.

The shared architecture pattern

| Layer | What the layer does | Why it matters now |

|---|---|---|

| Inventory | Records each AI use case, model, vendor, owner, and customer impact | Supports APRA-style lifecycle accountability and DTA-style use-case governance |

| Risk and approvals | Assigns risk tier, decision rights, and human gate thresholds | Prevents low-risk and high-risk uses from being treated as if they are the same |

| Transparency | Triggers customer or user notices when AI is part of the interaction or output | Supports EU-facing disclosure expectations and builds trust more broadly |

| Evidence | Captures prompts, inputs, outputs, approvals, overrides, incidents, and rationale where appropriate | Makes audits, disputes, and remediation possible |

| Resilience | Covers cyber controls, concentration risk, incident response, fallback, and rollback | Aligns with ASIC urgency and APRA’s concern about supplier dependency and operational resilience |

3. Transparency and customer notice

The EU AI Act clock matters because it forces a very practical product question:

Where exactly will the user be told that AI is involved?

That might be in a chatbot, a generated explanation, an automated communication, synthetic content, or a workflow where AI is shaping what a human sees next.

Many firms still treat transparency as legal text to add later.

It is not.

Transparency is a product surface. It has to be designed into channels, interfaces, scripts, and escalation paths.

Even if your immediate obligation is not EU-specific, this pattern is spreading because it is intuitively where trust goes next. People want to know when they are dealing with a machine, when content is generated, and when a human is still accountable.

4. Evidence, traceability, and replay

The moment a customer challenges an outcome, a partner escalates an incident, or a regulator asks what happened, the quality of your evidence becomes the whole game.

You need to be able to reconstruct:

- what the system did,

- what data or context it used,

- what the human reviewer saw,

- whether an override occurred,

- and how the issue was corrected.

This is the difference between “we have logs somewhere” and “we can support an investigation, dispute, or remediation process without panic.”

In regulated environments, the second one is the real standard.

5. Recovery, fallback, and concentration discipline

ASIC’s warning is not abstract. It is about a threat environment where AI compresses the time between vulnerability discovery and exploitation. APRA is also explicitly worried about concentration, opacity, and weak contingency planning around providers. (ASIC, APRA)

So the control stack also needs:

- vendor and concentration visibility,

- tested fallback paths,

- privileged access discipline,

- incident response playbooks,

- and a way to pause or roll back high-impact AI-enabled actions.

The governance model is not complete until the recovery path is designed.

The 10-star test for AI compliance

This is where the 10-star lens matters.

A 5-star compliance posture is one where nothing obviously bad has happened yet.

There is a policy. There is a committee. There is probably a spreadsheet. Someone says there is “human oversight”. The build feels acceptable from a distance.

But a regulated AI workflow should not be judged against a 5-star bar.

For fintech, the more useful minimum is 8-star behaviour:

- leadership can see the current AI inventory and the highest-risk exceptions,

- every consequential use case has a named owner,

- reviewers can genuinely stop or override high-impact outcomes,

- user-facing AI interactions have a clear notice pattern,

- incidents can be reconstructed without heroics,

- and critical vendors have a contingency story.

That is the difference between compliance theatre and compliance architecture.

What to do in the next 30 days

If I were helping a fintech leadership team respond to this stack today, I would start with five moves.

1. Build the AI register before building more pilots

List every current and proposed AI use case, including embedded AI inside third-party platforms and developer tooling.

2. Name one accountable owner per use case

Not a committee. A real owner.

3. Classify which workflows are customer-facing or decision-shaping

That is where transparency, human review, and evidence quality matter most.

4. Add one common control pattern

For high-impact workflows, standardise the same minimum pattern:

- approval gate,

- evidence captured,

- user notice where relevant,

- incident path,

- rollback or pause mechanism.

5. Review concentration and recovery for critical AI vendors

If one provider disappears, degrades, changes behaviour, or becomes a security issue, what keeps working?

The strategic point

The real opportunity here is not just avoiding fines, audit pain, or remediation cost.

It is building a fintech operating model that can adopt AI faster because trust does not have to be re-argued from scratch every time a new use case appears.

That is why this matters commercially.

The moat is no longer the model.

It is the discipline around the model.

When four oversight clocks all start pointing at the same design pattern, the winners are usually the firms that treat the pattern as infrastructure, not paperwork.

Related reading

- EU AI Act Countdown: Human Oversight Cannot Be A Checkbox - where the human-in-the-loop design challenge gets real.

- AI Washing Is The New Greenwashing - why public AI claims now need evidence and governance behind them.

- I Gave an AI Agent the Keys. Here Is the Trust Architecture. - what a constrained, accountable agent stack looks like in practice.

- The 10-Star Experience: Why Product and Engineering Need Legendary Test Cases - the foundational framework for mapping and testing delight-driven compliance.

Written by Haris Habib from Sydney, Australia | May 2026