AI washing is becoming the new greenwashing.

The pattern is familiar. A new technology becomes strategically important. Investors reward the companies that appear to be ahead. Marketing teams sharpen the language. Pitch decks get louder. Disclosure gets fuzzier. Then regulators ask the boring question that cuts through the whole story:

Can you prove what you claimed?

That is where AI has arrived.

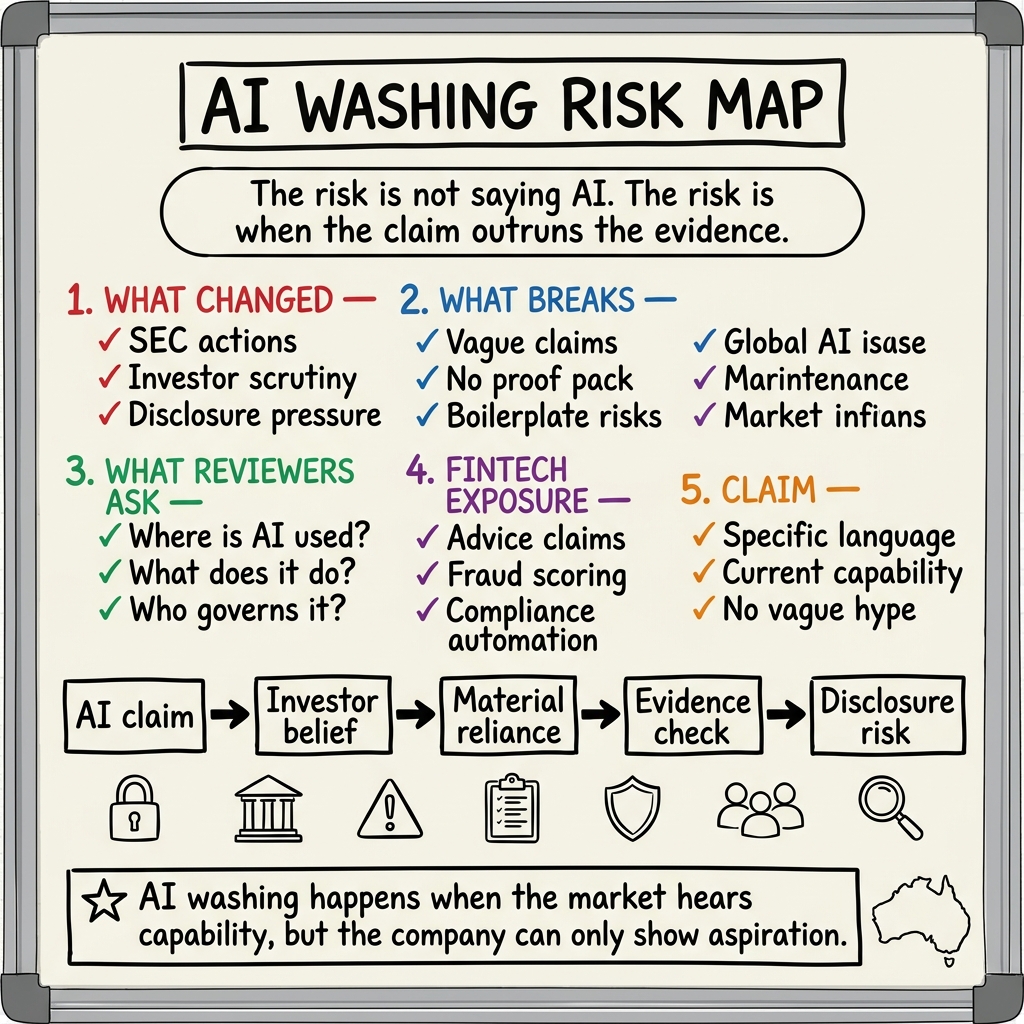

In March 2024, the US Securities and Exchange Commission settled charges against two investment advisers, Delphia and Global Predictions, for allegedly making false and misleading statements about their use of AI. The firms agreed to pay a combined US$400,000 in civil penalties. The SEC’s message was blunt: if an adviser claims to use AI in an investment process, the representation cannot be false or misleading. Public issuers making material AI claims also need to be careful. (SEC)

That was not an isolated warning. In October 2024, the SEC charged Rimar Capital entities and individuals over allegedly false claims about an AI-driven trading platform. The case involved nearly US$4 million raised from 45 investors and a US$310,000 settlement package. (SEC)

The lesson for fintech is not that every AI claim is dangerous. The lesson is that the gap between AI language and AI evidence is now a regulatory, investor, and procurement risk.

AI claims are becoming disclosure claims

AI used to be treated by many companies as a product-positioning word. Now it is becoming a disclosure word.

That changes the standard.

A company saying it is “AI-powered” may be making a claim about capability, cost structure, product differentiation, risk management, customer outcomes, or future growth. If that claim is material to investors, customers, or regulated buyers, it cannot simply be brand language. It needs a reasonable basis.

Former SEC Chair Gary Gensler put it directly in a September 2024 statement: companies making AI disclosures should remember that securities-law basics still apply; claims about prospects need a reasonable basis; AI risks should be particular to the company, not boilerplate; and companies may need to define what they mean by AI and explain how and where it is used. (SEC)

That point matters even outside the United States, because global investors and enterprise buyers increasingly read AI claims with the same discipline. They want to know whether the company is using AI in production, in pilots, in internal operations, in customer-facing decisions, or merely in the roadmap.

Those are very different things.

Why fintech is especially exposed

Fintech has more AI-washing risk than most sectors because AI claims often sit close to financial outcomes.

When a fintech says AI improves fraud detection, credit decisioning, compliance operations, personalisation, reconciliation, trading, or customer support, the claim may affect how investors value the company and how customers assess trust. It may also affect how banks, payment providers, insurers, and regulated partners evaluate the firm.

This is why “AI washing” is not just a marketing issue. It is a governance issue.

The riskiest claims usually sound like:

| Claim | What a reviewer may ask |

|---|---|

| ”Our AI detects fraud in real time.” | What model, what signals, what false-positive rate, what human escalation? |

| ”We use AI to automate compliance.” | Which obligations, which workflow steps, what evidence trail, what oversight? |

| ”Our platform is AI-native.” | Which parts are AI, which are rules, which are human operations? |

| ”AI improves underwriting or credit decisions.” | What data is used, how is bias tested, how are adverse outcomes reviewed? |

| ”We have proprietary AI.” | What is proprietary: model, data, workflow, evaluation, distribution, or UX? |

The claim is only as strong as the operating evidence behind it.

The SEC is moving from hype to evidence

The most important regulatory signal is not one single case. It is the pattern.

The SEC has already taken AI-washing enforcement actions. Its 2026 cyber-related exam priorities include reviewing controls to mitigate new risks associated with AI and polymorphic malware. And in December 2025, the SEC Investor Advisory Committee recommended that issuers define what they mean by AI, disclose board oversight mechanisms where applicable, and report separately on material AI deployment in internal operations and consumer-facing matters. (SEC, SEC IAC)

That does not mean every startup needs public-company-grade disclosure. But it does show where the standard is heading.

Regulators and sophisticated buyers are becoming less interested in whether a company says “AI” and more interested in whether it can explain:

- what AI is actually doing,

- where it is deployed,

- what data it depends on,

- what human controls exist,

- what risks are monitored,

- and whether public claims match internal reality.

That is the operating discipline fintechs need before the claim becomes material.

The practical test: can your AI claim survive diligence?

Founders do not need to remove AI from their language. They need to make the language more precise.

Before publishing an AI claim, teams should ask five questions:

-

Is the claim true today?

Not planned. Not implied. Not on the roadmap. True in the current product or process. -

Is the claim specific?

”Uses AI to summarise support tickets” is stronger than “AI-powered operations.” Specific claims are easier to defend. -

Is the claim evidenced?

There should be internal documentation, test results, workflow diagrams, model cards, evaluation results, or customer proof that supports the statement. -

Is the claim governed?

Someone should own the claim. Legal, compliance, product, engineering, and marketing should not be operating from different versions of the AI story. -

Is the claim matched by risk disclosure?

If AI is material to the business, then limitations, dependencies, data risks, vendor reliance, security exposure, and failure modes may also be material.

The companies that get this right will not sound less ambitious. They will sound more credible.

The fintech opportunity

There is a positive version of this story.

As AI language becomes cheaper, verified AI capability becomes more valuable. The strongest fintechs will be able to show not only that they use AI, but that their AI is deployed in ways customers, partners, and regulators can trust.

That means building a claim-to-control chain:

Marketing claim -> product behaviour -> technical evidence -> governance owner -> risk disclosure.

If those five things line up, AI becomes a defensible advantage. If they do not, the company is borrowing credibility from a technology it cannot yet prove.

The next wave of AI scrutiny will not punish companies for using AI. It will punish the gap between story and substance.

For fintech leaders, the rule is simple:

If it is in the pitch deck, it should be in the controls.